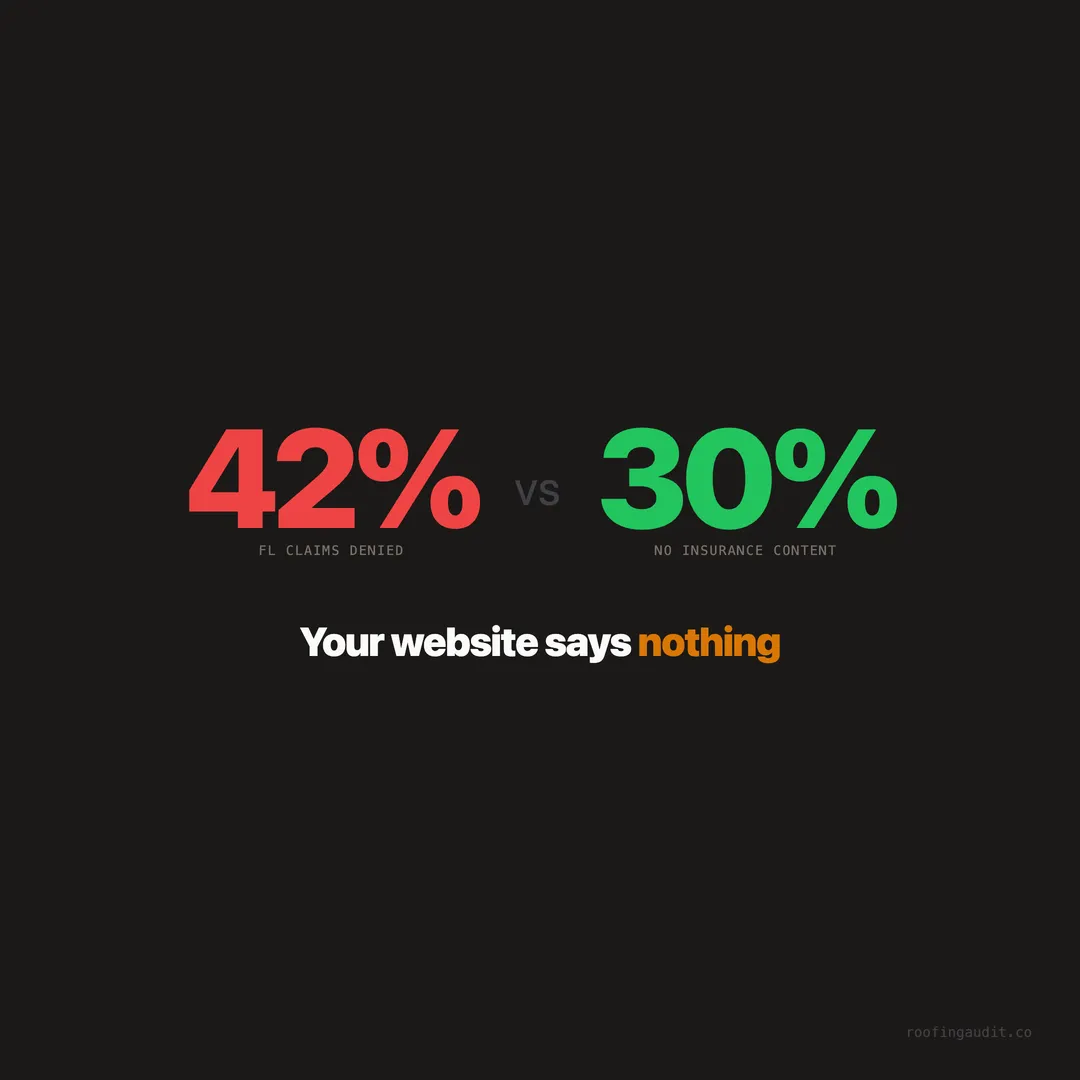

30% of Roofing Websites Have No Insurance Claim Content — In Florida Where 42% of Claims Get Denied

430 of 1,409 roofing sites offer zero insurance claim guidance. In FL where 42% of claims are denied, that's a massive lead magnet left on the table.

A homeowner in Fort Lauderdale files a hurricane damage claim. The insurance company sends an adjuster. The adjuster lowballs the estimate. The homeowner has no idea what’s reasonable, what’s covered, or what to do next.

She Googles “how to file roofing insurance claim Florida.” She finds three roofers. Two have no insurance content at all — just service pages and a phone number. The third has a full guide: how to document damage, what to expect from the adjuster, what the roofer handles, and a checklist for maximizing the claim.

She calls the third roofer. Not because they were cheapest or closest — but because they were the only one who helped her understand the process.

When we audited 1,409 roofing websites across Texas, Florida, and Georgia, 430 — 30% — had zero insurance claim content. No guides. No FAQs. No explanation of the claims process. Nothing.

In Florida — where 42% of hurricane insurance claims were denied in 2024 — that’s not a minor content gap. It’s a lead magnet sitting unbuilt on a shelf.

Why Insurance Content Is a Lead Machine

The roofing insurance claim is one of the most confusing processes a homeowner will ever face. Most have never filed one. They don’t know:

- Whether their damage is covered

- How to document it properly

- What the adjuster is actually evaluating

- Whether the adjuster’s estimate is fair

- What the roofer does vs. what the homeowner does

- How to appeal a denial

- Whether they need a public adjuster

Every one of those questions is a search query. And every search query is a homeowner ready to hire a roofer who can guide them through it.

The roofer who answers these questions on their website becomes the trusted advisor before the first phone call. The roofer who doesn’t answer them looks like every other contractor.

What a Strong Insurance Page Includes

From our analysis of top-scoring roofing sites, the most effective insurance pages follow a consistent structure:

Step-by-Step Claims Guide

Walk the homeowner through the process in simple language:

- Document the damage — take photos from multiple angles, include close-ups

- File the claim — call your insurance company within 24-48 hours

- Schedule a professional inspection — the roofer documents damage for the claim

- Meet the adjuster — the roofer should be present at the adjuster visit

- Review the estimate — compare the adjuster’s scope with the roofer’s assessment

- Approve the work — once insurance approves, the roofer begins replacement

- Final inspection — verify the work meets code and manufacturer specs

What the Roofer Handles vs. What the Homeowner Handles

Most homeowners don’t know that a good roofer will:

- Meet the insurance adjuster on-site

- Provide a detailed scope of work for the claim

- Supplement the claim if the adjuster’s estimate is too low

- Handle the permitting process

- Coordinate the warranty registration

Spelling this out on the website removes the homeowner’s biggest fear: “Will I be left dealing with insurance alone?”

Common Denial Reasons and How to Appeal

In Florida where 42% of claims are denied, showing homeowners why claims get denied — and how to appeal — positions the roofer as the expert.

Common denial reasons:

- “Pre-existing damage” — the adjuster attributes damage to age, not the storm

- “Cosmetic only” — the damage doesn’t affect function (the most disputed reason)

- “Maintenance issue” — the insurer claims the homeowner failed to maintain the roof

- “Filing deadline missed” — the homeowner waited too long

A roofer who explains these on their site — and offers to help navigate the appeal — wins the job before the competition even answers the phone.

Insurance Company Compatibility

Some roofers list the insurance companies they’ve worked with successfully. This is surprisingly powerful. A homeowner with State Farm seeing “We’ve successfully filed 200+ State Farm claims” feels targeted confidence.

The SEO Value of Insurance Content

Insurance-related searches are some of the highest-intent queries in roofing:

- “how to file roofing insurance claim”

- “roof damage insurance claim denied”

- “does homeowners insurance cover roof replacement”

- “roofing insurance claim process [city]”

These searches come from homeowners who already have damage and already have insurance. They’re not browsing. They’re buying. A page that ranks for these queries captures leads at the exact moment of maximum intent.

30% of roofing sites are invisible for these searches because they have zero insurance content. The schema markup gap compounds this — without proper markup, Google can’t associate the site with insurance-related queries.

Texas vs Florida: Different Insurance Landscapes

The insurance content should be state-specific:

Texas: Hail claims are the primary driver. Texas had 529 hail events in 2024. Hail claims are generally less disputed than wind claims — the damage is visible and measurable. The page should focus on hail documentation and timely filing.

Florida: Hurricane claims are more complex and more frequently denied (42% denial rate). Florida has additional layers: assignment of benefits (AOB) regulations, mandatory mediation, and a history of insurance company insolvency. The page should address denial appeals, public adjusters, and the unique Florida claims process.

Georgia: Growing storm exposure, less insurance complexity than Florida. The page should cover the basics with a focus on hail and wind damage documentation.

A roofer operating in multiple states should have separate insurance pages for each state. The claims process differs enough that a generic page won’t capture state-specific searches.

The Roofers Who Get This Right

In our audit, the roofing sites with insurance content consistently scored 15-20 points higher on the Website Quality Index than those without. The correlation is strong because insurance content signals:

- Expertise: “This roofer knows the claims process”

- Local knowledge: “They’ve worked with my state’s insurance system”

- Trustworthiness: “They’re not just going to take my money and leave me to fight insurance alone”

It also pairs perfectly with a storm damage gallery. Photos of completed insurance-approved jobs — with captions noting the insurance outcome — create a one-two punch of visual proof and process expertise.

Building Your Insurance Page Today

The page doesn’t need to be 5,000 words. It needs to answer the homeowner’s core questions:

- “Will my insurance cover this?” — Explain what’s typically covered (sudden storm damage) vs. what’s not (gradual wear)

- “What do I do first?” — Document, file, call a roofer

- “What will you do?” — Meet the adjuster, provide scope, supplement if needed

- “What if my claim is denied?” — Explain the appeal process

- “How much will I pay out of pocket?” — Explain deductibles honestly

Then end with a Free Inspection CTA: “Not sure if your damage is covered? We’ll inspect your roof and help you understand your options — at no cost.”

That page — combined with a storm gallery, certifications, and emergency repair info — turns a roofing website from a brochure into the most trusted source in the market.

430 roofing sites in our audit are missing it. The ones that aren’t are answering the phone while their competitors wait.

Keep reading

Want to know your score?

Drop your URL — full report in 48 hours.

We're on it.

Report in your inbox within 48 hours.